Do you still believe in PLG?

The never-ending PLG-SLG saga of B2B SaaS

The recent news of the layoffs and PLG-SLG prioritization in B2B SaaS have inspired me to share my personal thoughts on the matter. I understand that this topic is complex and multifaceted, but I believe it is important for people to express their opinions and engage in healthy debate. I want to stress that this post is solely my own perspective and I welcome alternative viewpoints and discussions. I have tried to incorporate those viewpoints via reviewer comments throughout the post. Many thanks to Francois Dufour, Chris De Vylder, Alex Poulos, and Anoushka Vaswani for their review and thoughtful comments. We’ve all recently read the news of layoffs in the tech Industry. If you pay close attention, a theme is evolving for late-stage B2B SaaS companies.

Many of them, as they continue to grow and evolve, Airtable, Brex, and Snyk, to name a few, have turned their attention toward the enterprise market by disproportionately laying off growth and self-serve teams; and curtailing their investments in Product-led Growth (PLG).

This shift towards larger, more established companies has sparked controversy, with some arguing that it prioritizes short-term profits over long-term growth. We’ve seen this happen before when companies like Dropbox and Slack swung the GTM pendulum to one extreme (Sales-led growth or SLG), only to correct it later.

I don’t believe the pendulum needs to swing so wildly on either side for B2B SaaS, PLG or SLG, even if you are going upmarket. Most well-run B2B SaaS organizations of the future will establish harmony between the two.

Business Case for PLG

There are many articles on the business case of PLG, so I’m not going to dive into the details. My primary question is: are we seeing a shift in the business case for PLG?

Users vs. Buyers: The consumerization of enterprise led to the birth of PLG. With PLG, the user can start using and getting value from the product immediately. The users also play an influential role in the buying process at the workplace. Do we see that changing soon? This trend will get more and more normalized in the next decade as more Millennials and Gen-X enter the workforce.

[Reviewer’s note: Do we see that changing soon? “Not necessarily and I for certain hope it doesn't change, but it has led to a fragmentation of business tools that have become unwieldy in some cases and a call from senior execs to consolidate. As a PLG business, you need to be able to counter that, especially if your "competitors" are more top-down and the time to assess which vendors should survive is limited in indiscriminate cost-cutting exercises.]

Network Effects: Most PLG products (team-based, organization-based) become more valuable to the user as more people use the product. This network effect creates a virtuous cycle of growth, making it more scalable than SLG, as it relies less on the ability of the sales team to generate leads and close deals. During economic downturns or recessions, this should help the organization be more profitable and not the other way around.

Lower CAC: Due to network effects, customer acquisition costs for PLG products are considerably lower. And this shouldn’t change now. Do I see unit economics changing for PLG products in the near term? Yes, but that will equally impact SLG products as well.

The business case for PLG is still considerably strong, so what is the origin of PLG anxiety?

PLG vs SLG Profitability

Tomasz Tunguz recently wrote an article about PLG vs SLG profitability in a post-covid world. He observes that while PLG companies were more profitable pre-Covid, their profitability is 5-10% less than SLG companies in a post-Covid world.

And he observes that the diff primarily originates from the following:

“PLG companies R&D spend hasn’t produced new business at the same rate as a dollar invested in sales & marketing post-Covid.”

The majority of the diff stems from the increased spending in R&D for PLG Companies:

Since there is a renewed focus on profitability in a post-Covid world, this has been construed as SLG companies being more profitable. Tomasz Tunguz highlights two areas where SLG companies have advantages (for now):

PLG companies tend to focus more on SMB vs. Enterprise, and SMBs are more impacted during the recession.

Much easier for SLG companies to adjust resources and processes for increased profitability.

So, companies like Airtable, Brex, Snyk, and Asana, which are primarily PLG-led, are reducing their investments in PLG and increasing their investments in SLG to move up-market and increase their profitability.

I am not questioning the investments in SLG. I am disputing the divestiture from PLG (and/or small business) as an excuse to go up-market. I believe this is short-term myopia. Why?

[Reviewer’s Note: “You can "juice" top-down selling much more effectively, vs. a PLG motion where investments pay off over time, but in a more consistent way. It's also a move to placate boards, who believe this will drive results. My view is that many will have hangovers a year down the road as they figure out that driving business through traditional DG channels isn't as effective or scalable.”]

[Reviewer’s Note: “Currently, what we are seeing on the growth side is extreme headwinds for every prosumer tool in their portfolio right now (some of the highest-quality PLG companies out there). In this environment, any company that hasn't added a meaningful enterprise motion is really struggling now. The lesson we are learning is that in this climate anything that isn't 1) supercritical, 2) a daily-usage product, and 3) has some visibility into procurement will likely struggle. We are more likely going to be in a "re-bundling" environment vs. "un-bundling" for the foreseeable future. Things will shift back and forth between economic cycles but having an effective enterprise motion is quite nice through a macrocycle.]

Reason 1: Enterprise buying behavior is changing

More and more enterprise companies are getting comfortable using software not approved by a central buyer in the organization and this will only change more due to a tech-savvy workforce and consumerization of the enterprise. Enterprises will buy software in the future using a combined PLG+SLG motion. OpenView Partners talks about this evolution here:

[Reviewer’s notes: “Yes and no in my view. For small transactions yes, but in this climate, even $100K transactions get scrutiny and the CFO goes to the senior person to get justification.”]

Reason 2: Small Businesses comprise a significant portion of the US GDP

Small businesses generate 44% of the US economic activity. Though their share has fallen from 48% in 1998 to 44% in 2014, over the same period their share has grown 25% in real terms. According to Statistica, small businesses are forecasted to spend 725 billion dollars on IT services in 2023, vs. 545 billion by medium-sized businesses. Globally, 99% of the businesses are small businesses, and employ 70% of the workforce.

Though small businesses are impacted the most during recessions, they are also the fastest to recover when an economy rebounds from a downturn.

Reason 3: Small Businesses of today are the Enterprises of the future

This is very true, especially for companies like Snyk, Asana, Airtable, and Github, which primarily sell into the tech sector. Google, Facebook, Amazon, Microsoft, etc. were all small startups at some point in the past and now are technological behemoths. Approximately, 30% of small businesses of today will survive and become enterprises of the future.

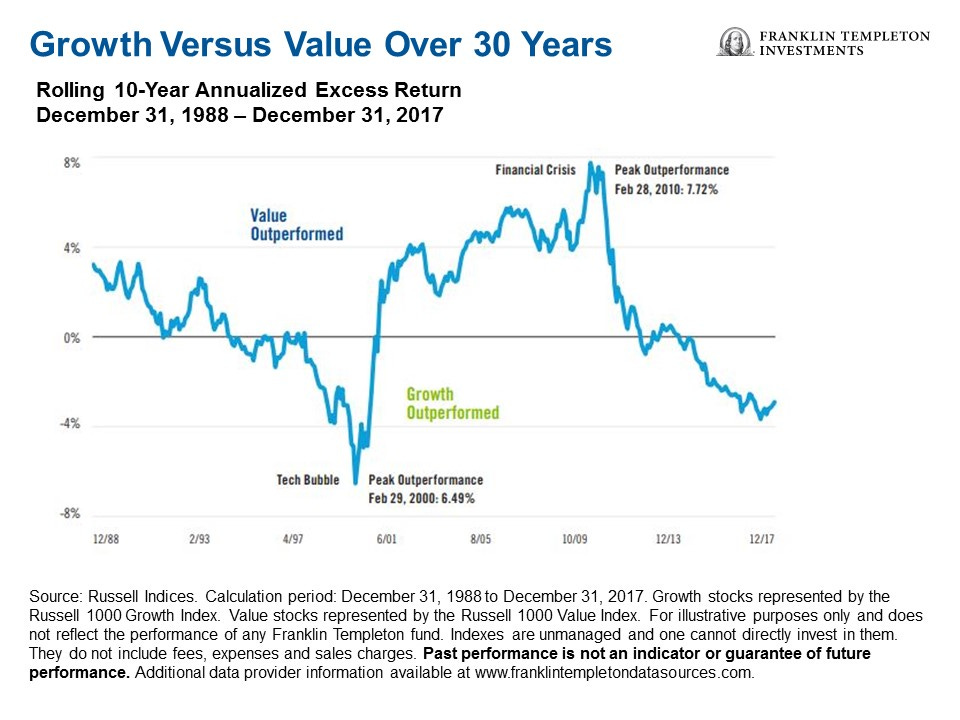

Reason 4: The Growth-Value Cycle

Last year, it was all about growth - growth at all costs. No one cared about your net income statement. This year “growth” has gone out of fashion. It is all about profitability and positive cash flow. What changed in the last 12 months: Your business model? Your customer needs? Product market fit? Your employees? No! It is the stock market and how companies are valued - an intangible metric which has nothing to do with your product or customers.

This phenomenon is not new. The growth-value cycle has been happening for the last 35 years. A year from now, growth will become the most important metric, and then you have to redo your strategy again - all those experts you laid off, you have to rehire them. Why? PLG products grow at a much faster rate than SLG companies, as documented by Openview here:

[Reviewer’s note: “I would say the best grow at a consistent, solid pace for much longer, because the foundation of a PLG business is much more sound than a pure SLG business, given that it's rooted in a product that is well-liked.”]

Vox Populi, Vox Dei?

"Vox Populi, Vox Dei” is a Latin phrase that translates to "the voice of the people, the voice of God." It is often used to express the idea that the will or opinion of the majority holds great power and authority.

But if you read the entire quote:

“Do not listen to those who say the voice of the people is the voice of God, since the tumult of the crowd is always close to madness."

Don’t follow the eccentricity of the masses. Or, what separates you from the rest? Atlassian never wavered from their PLG path in spite of everyone arguing that an enterprise won’t buy without talking to a person. Look where it took them. Or learn from Notion who is using the downturn to play offense, and increasing their investments while everyone is cutting corners for a positive cash flow.

Being Great!

Great companies are those that have a clear vision for the future and are willing to make long-term investments to achieve it. They understand that true success is not a short-term gain, but a marathon, not a sprint. They are able to tune out the noise of short-term pressures and stay focused on their goals, even in the face of adversity. They have a deep understanding of their customers and industry, and they use this knowledge to create products and services that truly meet the needs of their customers, not just what is trendy or popular at the moment.